HELOCs (Home Equity Lines of Credit) are widely used. Simply having one makes many people more comfortable. My wife and I had a standby HELOC for many years – ready to use as a convenience or in an emergency. Luckily that emergency never happened, but we felt well prepared knowing we had ready access to a substantial amount of cash that could be used for anything we needed. When I was a financial advisor, a HELOC was on my checklist to discuss with every client – at least those who were prudent with their money.

ReLOC: A Retirees Line of Credit

Is there a better alternative for homeowners over age 62? A ReLOC may be a far better choice for many retirees. ReLOC is a nickname that stands for either Retirees Line of Credit or Reverse Mortgage Line of Credit. While ReLOCs share many features with HELOCs, three unique features make a ReLOC a line of credit designed for retirees:

- The amount you can access grows every month

- You don’t have to make payments until you permanently leave your home

- The loan can’t be canceled, reduced, or frozen as long as you keep up with basic mortgage obligations (property tax, homeowner’s insurance, basic maintenance, and Homeowner’s Association dues).

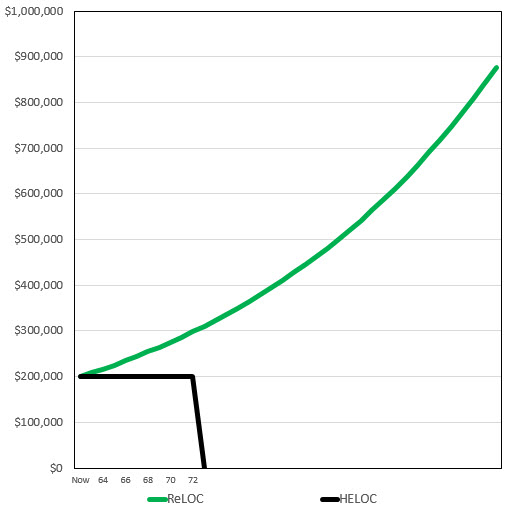

Here’s the borrowing limits for a ReLOC and a HELOC for a 63-year-old in a $400,000 house who lives to age 99:

ReLOC borrowing limit starts at $200,000 and grows at 4%. HELOC starts at $200,000 and lasts until the draw period ends at 10 years.

The scenario shows a 63-year old homeowner who qualifies for a HELOC or a ReLOC, each with an initial borrowing limit of $200,000. That’s half the value of their $400,000 home. While an existing mortgage or HELOC may be refinanced into a ReLOC that scenario isn’t discussed in this brief note.

HELOC Choice

The HELOC, shown by the black line, allows borrowing up to $200,000 during a 10 year draw period. It may require monthly interest payments on any current balance. The HELOC in the picture has no balance at the end of the 10 year draw period so the loan terminates. The homeowner may or may not be able to qualify for new HELOC then.ste

If there is a balance at the end of the draw period the loan enters the repayment period. Fixed monthly payments would be set up to pay both interest and principal to pay the loan off over 20 years. If the loan balance was $200,000, the required payments would be $1,212 a month ($14,544 a year) at a 4% interest rate. With those payments it would take until the homeowner is 93 years old to pay it off. The HELOC repayment period works the same way as a traditional mortgage: no draws and can’t skip payments. The HELOC’s flexibility ends when the loan switches from the draw to the repayment period.

ReLOC Choice

This homeowner also has a choice of a ReLOC with a $200,000 borrowing limit. They could withdraw as much as $120,000 in the first year (60% of the borrowing limit). The additional $80,000 is available on the first day of the loan’s second year.

The borrowing limit – the accessible amount of cash – grows every year at the ReLOC’s loan rate, whether they have borrowed from it or not, and whether the home has appreciated or not. The borrowing limit’s growth has been called the ReLOC’s Hidden Value. Like the HELOC, this is a variable rate loan and is shown with a 4% growth rate.

By the time our homeowner turns 80, if they had not tapped their $200,000 ReLOC they could withdraw $400,000. Or nearly $600,000 at age 90, and $800,000 at age 97! Surprisingly, the ReLOC’s growth may be both stronger and more reliable than a retiree’s investment portfolio – that’s a topic for a future blog post. Of course, the ReLOC’s growth is increased access to cash based on the home’s equity, while a portfolio’s growth provides “new money”.

A key fact is no payments are required as long as they live in the home. The homeowner may find making payments very beneficial. A payment both reduces the loan balance and increases the amount that grows and can be borrowed again. More flexibility and homeowner protection stems from the fact that the maximum amount owed on the loan is limited to what the house is worth when the homeowners leave it.

A “Standby ReLOC” that is set up and held in reserve could be an emergency fund to deal with risks that show up late in life. Health-related risks always come to my mind – accommodations so I could stay at home, have home care, pay entry fees to a good continuing care retirement facility, medical treatments I choose rather than what my insurance plan allows, going to a specialist, … whatever is needed. The longer I live the more exposure I have to a variety of risks besides health-related ones – hits to the stock market, interest rates staying too low or shooting way up, high inflation pushing my costs up, a family member who needs help, or loss of SS and pension income if my spouse dies before me. The reassurance I felt having an emergency fund when I was working would now come from the ReLOC’s growing access to cash.

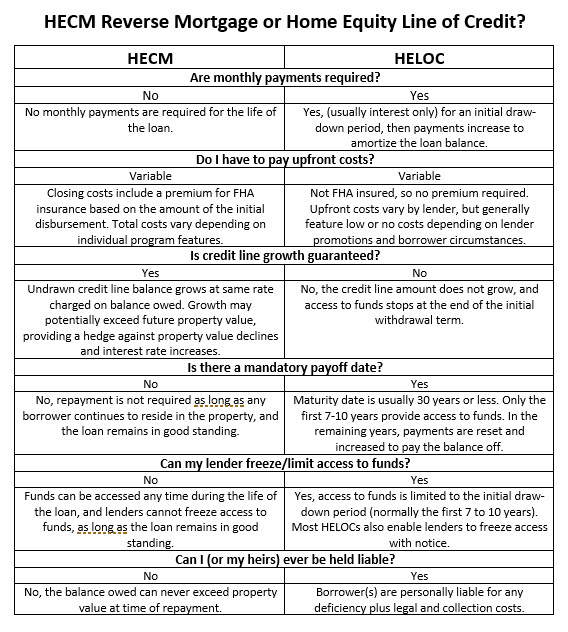

Beyond these standby risk reduction steps, financial planning studies have shown a variety of ways to use a ReLOC to improve lifetime spending, increase estate size, and sometimes both spending and estate size together. Other posts on this blog describe many of these. Here’s a comparison of ReLOC’s and HELOCs:

Here’s a comparison of ReLOC’s and HELOCs:

Recent Comments