Wade Pfau, a leader in retirement research, reported on research in “The Hidden Value of a Reverse Mortgage Standby Line of Credit”, an article that appeared on AdvisorPerspectives.com in December 2014. It is attached here with permission from Wade and Robert Huebscher of Advisor Perspectives. For more about and by Wade, see his blog at retirementresearcher.com.

Wade says: “Several recent research articles published in the Journal of Financial Planning have investigated how opening a standby line of credit through a reverse mortgage and strategically spending from this line of credit can help improve the sustainability of retirement income strategies. In this article, I show that the benefits of opening a home-equity conversion mortgage (HECM) line of credit extend beyond meeting spending needs.

With the current HECM rules, those living in their homes long enough could reap a large windfall when the line of credit exceeds the home’s value. This potential windfall is amplified by today’s low interest rates. Even if the value of the home declines, the line of credit will continue to grow without regard for the home’s subsequent value.

Combining this with the fact that a HECM is a non-recourse loan means that the HECM provides a very valuable hedging property for home prices.”

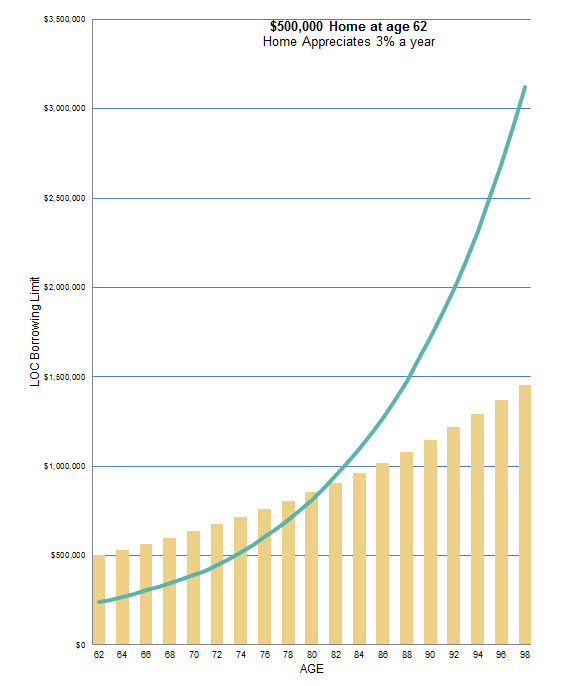

If a 62-year old homeowner took out a line of credit Wade’s analysis shows that “the probability that a line of credit could grow to be worth more than the value of the home … exceeds 50% by age 82 and 90% by age 86.”

The graph gives you an intuitive view of the results:

Wade continues by saying “The HECM program provides a way to create liquidity for the home, which is otherwise an illiquid asset. Removing the constraint about how home equity can be used affords a more efficient retirement-income strategy.

Even if that line of credit does not end up being used to meet income needs, its growth could provide a way to leave a larger legacy at death. The HECM is non-recourse, and mortgage insurance premiums are paid so that the lender does not lose after having paid more to the borrower than the home is worth. In this sense, the mortgage insurance premiums can be viewed as insurance against a fall in home prices if one lives sufficiently long.”

Building on Dr. Pfau’s analysis, how else might the Standby Line of Credit be used? While there are numerous ways, some are:

“Well-funded” homeowners – the more affluent – expect to have sufficient assets to meet their retirement spending. A Standby Line of Credit as a safety net might serve them well for unplanned expenses. Health-related issues certainly come to mind, with examples of extended in-home care, expensive home accommodations, or funding a move to a nursing home for either the first or second spouse to leave the home.

“Financially constrained” homeowners may use the line of credit to improve regular cashflow in a variety of ways such as augmenting investment portfolio withdrawals, paying off traditional mortgages or delaying the start of Social Security benefits.

“Underfunded” homeowners may need the line of credit to meet basic living expenses – the historic “last resort” use of reverse mortgages.

1 reply »