Reverse mortgages provide access to cash. Cash is the most flexible financial resource of all. In turn, access to cash makes a reverse mortgage a very flexible resource. Many homeowners could qualify for an FHA Home Equity Conversion Mortgage (HECM).

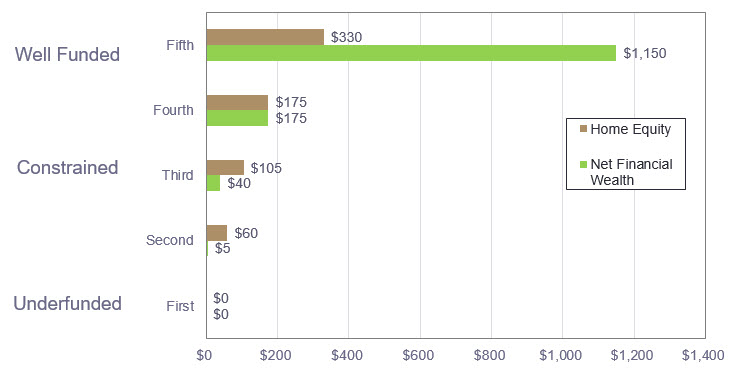

Steven Sass, a research economist at the Center for Retirement Research at Boston College, in his recent research brief “Is Home Equity an Underutilized Retirement Asset?” observed that while “retirement planning generally focuses on the use of financial assets,” he finds that “home equity is the largest store of savings for most households entering retirement.” And indeed, “for many households, particularly those with less wealth, home equity is larger than financial assets.” He analyzed home equity and financial wealth across households ages 65-69 for 2012 and expresses it in thousands of 2015 dollars.

For financial planning purposes, I overlay the concept of how adequately funded a homeowner is for retirement. “Fundedness” reflects how well a family’s financial resources match their retirement needs and desires. Many in the top wealth quintile would be Well Funded, as would part of the third and fourth wealth quintiles. Constrained and Underfunded describe a broader range of households.

While the distribution of wealth is not surprising, it provides context for appreciating the range of homeowner’s needs and how their home equity may contribute by using a reverse mortgage.

The value reverse mortgages could bring to the aging US population starts with the breadth of users and uses. The value and breadth also challenge homeowners, financial professionals, and the reverse mortgage industry to find good matches between an individual homeowner’s situation and their highest and best use of a reverse mortgage.

Recent Comments