The CFPB released a report on August 24 titled “Issue Brief: The costs and risks of using a reverse mortgage to delay collecting Social Security”. On a quick glance, the 26-page report seemed well written and documented (58 footnotes!). The analysis itself also appears to be carefully done. However, a considered reading finds the report suffers from silent and critical omissions across a variety of important factors. Those Sounds of Silence are loud and pervasive. The end result is a very misleading picture which can lead to many, perhaps most, Social Security beneficiaries making bad decisions about their Social Security in general, and particularly when combining it with another financial resource they may have such as home equity.

Many Social Security recipients will be best served by claiming Social Security early. Broadly speaking, they seem to be those for whom the CFPB analysis might apply. If Social Security is your only or primary retirement resource and you are single, you will often be best served by starting it as soon as possible. However, if other financial resources are available, including IRAs and 401(k)s, delaying may serve you better. The greatest of many flaws in the CFPB analysis is not even mentioning the diversity of retirement resources and preparedness seen across the range of Social Security recipients.

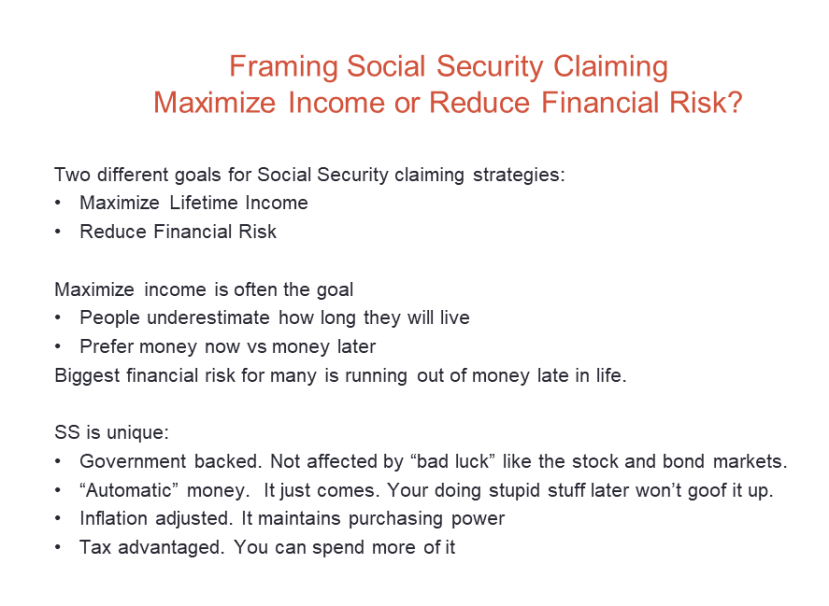

Many people approach the Social Security claiming decision from the perspective of maximizing lifetime income. A different perspective is reducing lifetime financial risk. Often either approach leads to the same result – delay Social Security, at least for a while. The risk perspective focuses on longevity. If you expect to live a very short time you tend to want the money as early as possible (unless you are married and your spouse’s longevity comes into your picture.)

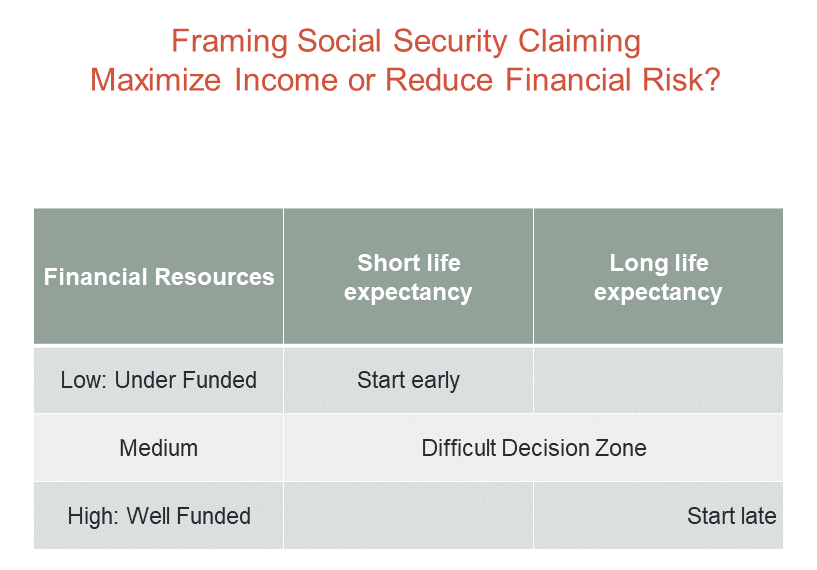

Here’s a small decision chart. The easy decisions fall in two places: (1 ) if resources are low and you don’t expect to live very long, and (2) the opposite, with lots of financial resources and you expect to live a long time.

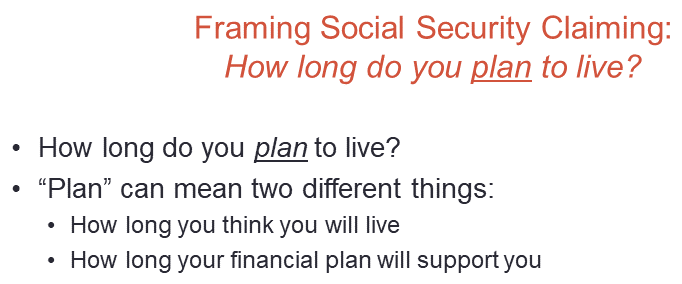

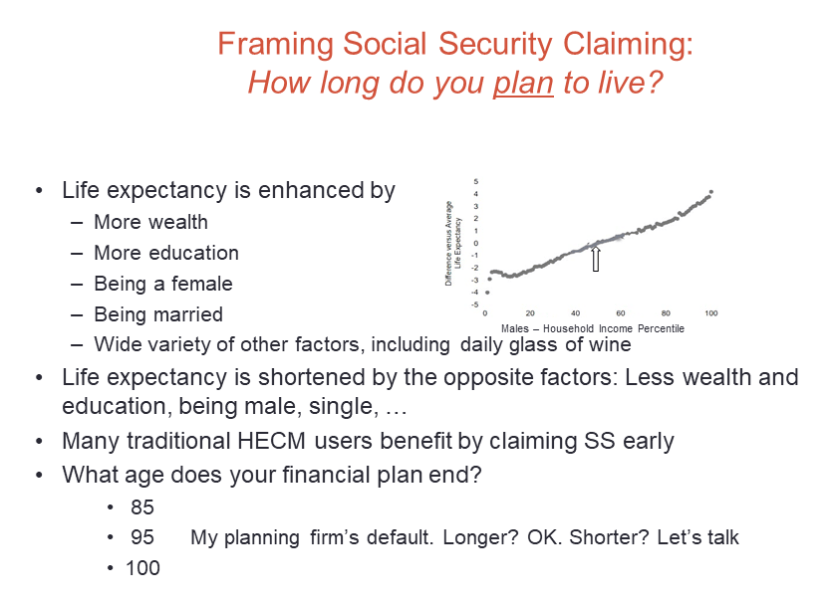

“How long do you plan to live?” A classically ambiguous question. What does “plan” mean?

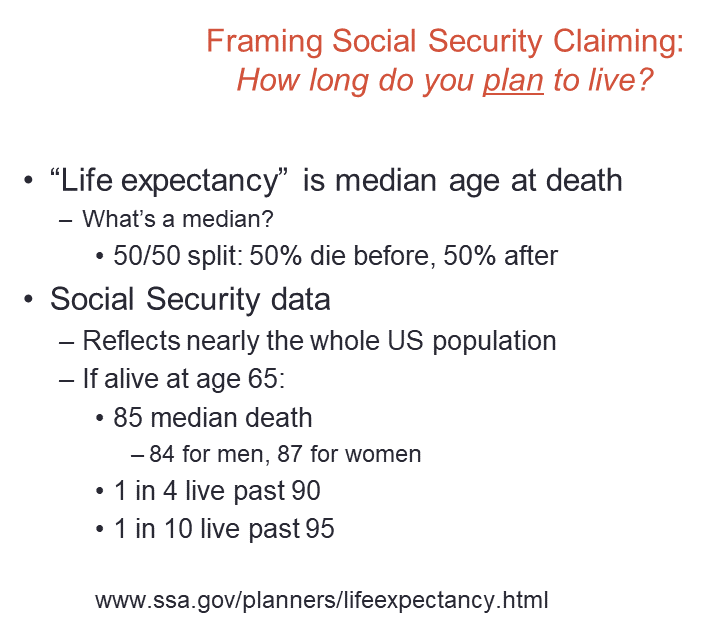

Life expectancy is a technical term. It is a median.

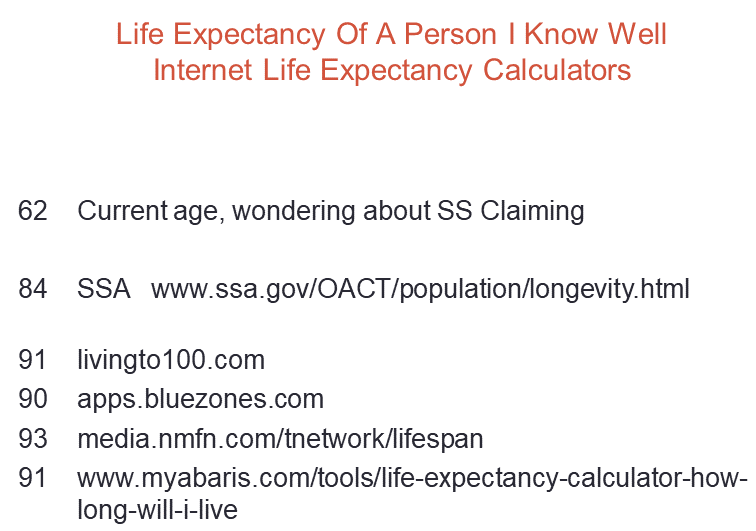

Medians don’t tell you anything about the range of ages – how many people die very early or very late. Many factors affect life expectancies – some inherited, some are about choices you will make, and what has happened so far in your life. I pretended I was age 62 (which was true some years ago) and tried 5 web-based life expectancy calculators. The Social Security estimate was well below the calculators that included other factors in my life, like the fact I’m married. It was

Wealth, education, sex, seat belt use, and many other things influence how long you may live as described below. The little line chart in the corner is from a Journal of Financial Planning paper by David Blanchett, Michael Finke, and Wade Pfau in the Journal of Financial Planning “Planning for a More Expensive Retirement.” The chart here was simplified to show the relative life expectancy for males as household income goes up. From low to high income there is an 8-year spread in life expectancy! Income is just one of many factors affecting life expectancy and should be included in an informed Social Security strategy.

Longevity is the key risk. It serves as a risk amplifier or risk multiplier. Wade Pfau says it well: “longevity risk becomes the overarching risk, because the longer a retirement lasts, the greater are the chances that other forms of risk will manifest. Increased longevity means more time for another financial crisis, more time for inflation to compound, increased chances for an expensive health problem, etc.” Dirk Cotton, on his blog The Retirement Café, has an excellent discussion of retirement risks in a series of posts including the interplay of longevity with Social Security claiming.

Longevity is the key risk. It serves as a risk amplifier or risk multiplier. Wade Pfau says it well: “longevity risk becomes the overarching risk, because the longer a retirement lasts, the greater are the chances that other forms of risk will manifest. Increased longevity means more time for another financial crisis, more time for inflation to compound, increased chances for an expensive health problem, etc.” Dirk Cotton, on his blog The Retirement Café, has an excellent discussion of retirement risks in a series of posts including the interplay of longevity with Social Security claiming.

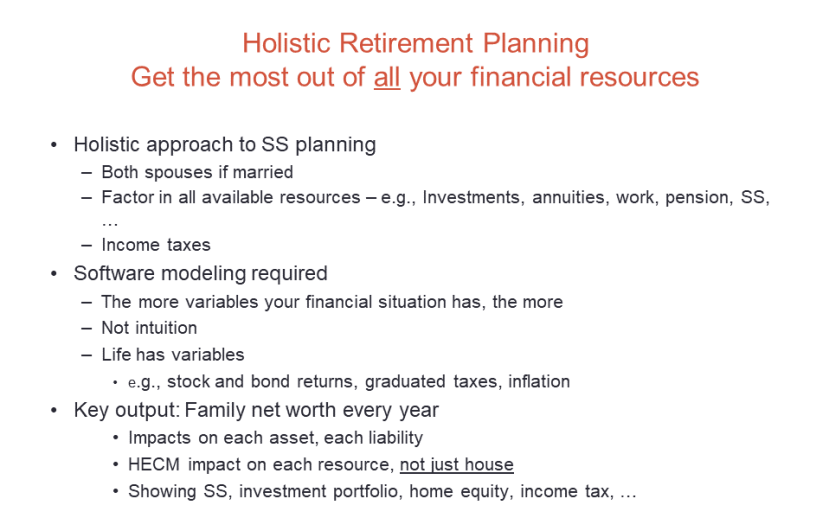

Many people have several resources contributing to retirement spending, including an IRA or 401(k), other investments, further work income, equity in your home, a pension and even a potential inheritance. All your available financial resources will play a role. The CFPB analysis considered only home equity, and for home equity, only one of several ways to use cash from a reverse mortgage.

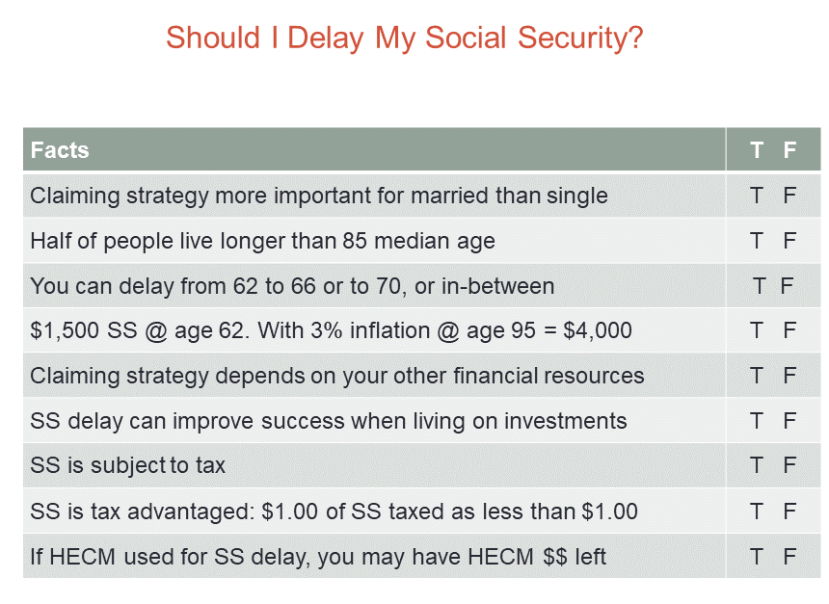

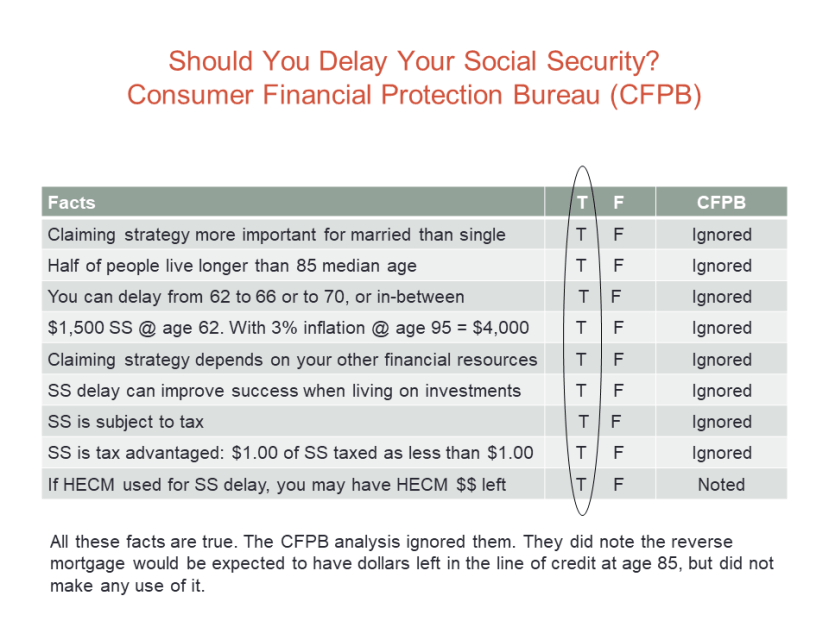

Quiz about Social Security Claiming

Let’s pull this discussion together to wrap it up. Here’s a quiz about Social Security claiming. Some key facts and features every SS beneficiary should be aware of. Which do you think are true?

They are all are true. There is a whole range of factors you should consider to make an informed decision about starting your Social Security. The CFPB ignored eight of them. They noted the last factor but did not comment on whether it was useful or not.

Conclusion

All in all, the CFPB analysis is silent on far too much. That silence creates a huge hole in the entire analysis and leads to the wrong conclusion far too often. As noted above, there are many fundamental flaws in the report. In closing I’ll mention just two from the list above:

- Only the half of population is included – the half who die earliest (by the median age). The half who live longest are ignored and are who can benefit most from SS delay.

- Those who were included never received any inflation adjustment to their SS payments over 24 years! However, they did have inflation built into the reverse mortgage “cost”. Is it a wonder that the cost-benefit analysis suffered?

In spite such a flawed analysis, the report (as planned) gets the right answer to the claiming decision for some Social Security recipients – those who in general are best served by claiming early. In particular, many if not most traditional users of reverse mortgages should start early – perhaps when they stop work. But getting the right answer for the wrong reason is not acceptable. In general, the report does a disservice to Social Security recipients and to those who should consider using a reverse mortgage to improve their retirement.

The analysis is completely silent on half of the population – the half who live longer than the median. It misses the best answer for anyone who would benefit by delaying Social Security. In particular, those might combine delayed Social Security with reverse mortgage funds to improve their retirement.

In my more acerbic moments, it is tempting to say that the CFPB analysis applies only to a non-existent retiree: one who gets Social Security but never gets inflation adjustment and dies early.

For thoughtful and more tactful comments on the CFPB report, some by other members of the Funding Longevity Task Force I serve on, see a recent article by Robert Powell in USA Today.

Recent Comments