Recent research has shown six unique methods of combining portfolio and reverse mortgage withdrawals can boost spending (Pfau, 2016a, 2016b). Each method substantially improved lifetime spending. And counterintuitively, potentially estate size as well. Barry Sacks and Mary Jo Lafaye (Sacks and Lafaye, 2016) recently published a case study demonstrating the elegantly simple coordinated strategy introduced by Barry and Stephen Sacks in the Journal of Financial Planning (Sacks and Sacks, 2012). The case study allows you to “see” how the strategy works. The case study description is available here: Sacks and Lafaye, along with a supporting PowerPoint slide deck (Sacks Coordinated Strategy Presentation).

Retired homeowners conventionally live on their investment portfolio. They turn to a reverse mortgage only if they run out of money. For them a reverse mortgage is a “last resort.” “The coordinated strategy is very simple: In each year directly following a year of negative investment returns in the portfolio, the portfolio is not drawn upon. Instead, the reverse mortgage credit line is drawn upon for the retiree’s income. In this strategy, the reverse mortgage credit line is used to offset the “adverse sequence of returns.”” “When the credit line is used in coordination with the portfolio, instead of as a last resort, it prolongs the life of the portfolio and greatly increases the net worth (and the legacy) of the retiree.” (Quotes taken from the case study).

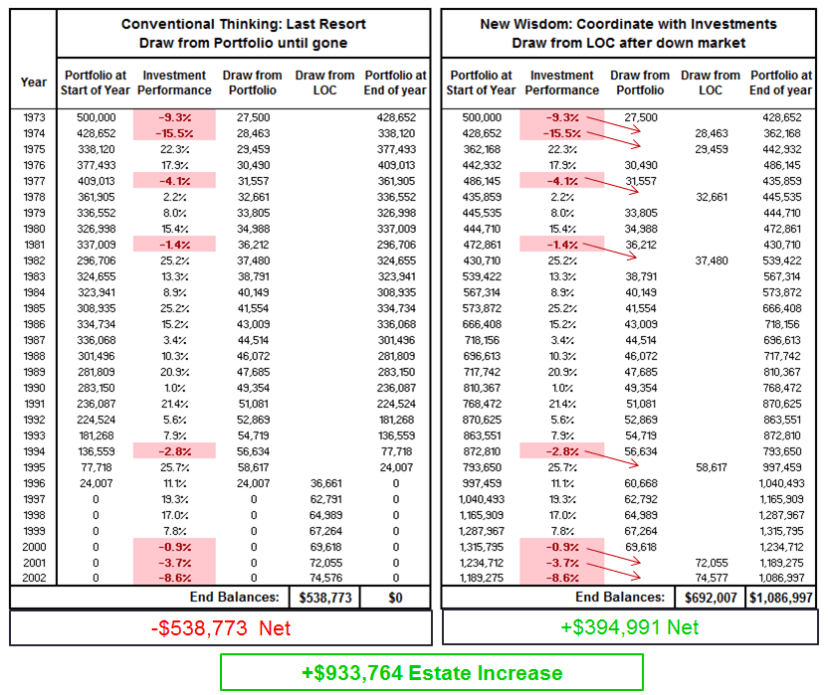

The case study uses a $500,000 50/50 equity/bond portfolio starting in 1973. It runs for 30 years with an initial 5.5% withdrawal rate increasing at a 3.5% inflation rate. Here’s what happens year-by-year:

With no reverse mortgage the homeowner ran out of money in the middle of 1996, leaving 6 more years to go. In contrast, with the reverse mortgage they put in place early in retirement their spending was fully funded through the 30th year.

Using the simple coordinated strategy has dramatic results: they don’t run out of money. Their estate size increases over $900,000. Rather than the portfolio exhausting in the 24th year, it lasts through the 30th year, with a $1,000,000 balance

The irony is this 30 year period was very rewarding if people were investing rather than living on a portfolio. A $500,000 portfolio at the beginning of 1973 grew to $5.8 million by the end of 1997 if left untouched. But note that this 30 year period’s three decades started out weak, then were good, and finally great. The first decade started in the ’70s with the Arab oil embargo, and suffered 9% and 15% declines in the first two years. The middle decade had “good” markets. The last decade brought the euphoria of the dot.com era, ending with worries about Y2K computer failures when the calendar turned to 1/1/2000.

But note that this 30 year period’s three decades started out weak, then were good, and finally great. The first decade started in the ’70s with the Arab oil embargo, and suffered 9% and 15% declines in the first two years. The middle decade had “good” markets. The last decade brought the euphoria of the dot.com era, ending with worries about Y2K computer failures when the calendar turned to 1/1/2000.

For retirees in withdrawal mode the order of market returns matters, and can matter a lot. Combining the first two year’s portfolio declines of 9% and 15% with the withdrawals reduced the $500,000 portfolio to $338,493 at the end of the second year. That hole turns out to have fatal lasting impact, despite portfolio gains of 22% and 18% in the next two years! The portfolio was out of money with six and a half years to go, as shown in the red line: “Last Resort – ReLOC” (ReLOC is Reverse mortgage Line Of Credit).

It is illuminating to look again at just at the first two years, 1973 and 1974, with portfolio drops of 9% and then 15%. If they used reverse mortgage draws to skip portfolio withdrawals after each of just those two early bad years the portfolio would support spending for the rest of their retirement! And at the end there would even been several years of spending left in the portfolio ($247,744)! Sequence of returns risk, the risk to retirees in withdrawal mode posed by bad market returns early in retirement, can be surprisingly large! (Pfau, 2013).

This case study usefully illustrates how the coordinated strategy works. The strategy is simple to state and simple to use. It is a direct attack on investment risk, and especially sequence of returns risk. Individual homeowners can do this! The homeowner needs to take out a reverse mortgage line of credit as early as possible. Naturally the larger the reverse mortgage line of credit is the more it can help the homeowner.

References:

Pfau, Wade. 2013. “Lifetime Sequence of Returns Risk.” https://retirementresearcher.com/lifetime-sequence-of-returns-risk/

Pfau, Wade. 2016a. “Incorporating Home Equity into a Retirement Income Strategy.” Journal of Financial Planning 29 (4): 41–49.

Pfau, Wade. 2016b. “The Retirement Researchers Guide: Reverse Mortgages” Forthcoming book.

Sacks, Barry H., and Stephen R. Sacks. 2012. “Reversing the Conventional Wisdom: Using Home Equity to Supplement Retirement Income.” Journal of Financial Planning 25(2): 43-52

Sacks, Barry, and Mary Jo Lafaye. 2016. “Case Study.” In Giordano, Shelley. 2016 “An Alternative Asset to Buffer Sequence-of-Return Risk in Retirement.” The Retirement Management Journal, 6(1): 17-26.

Recent Comments