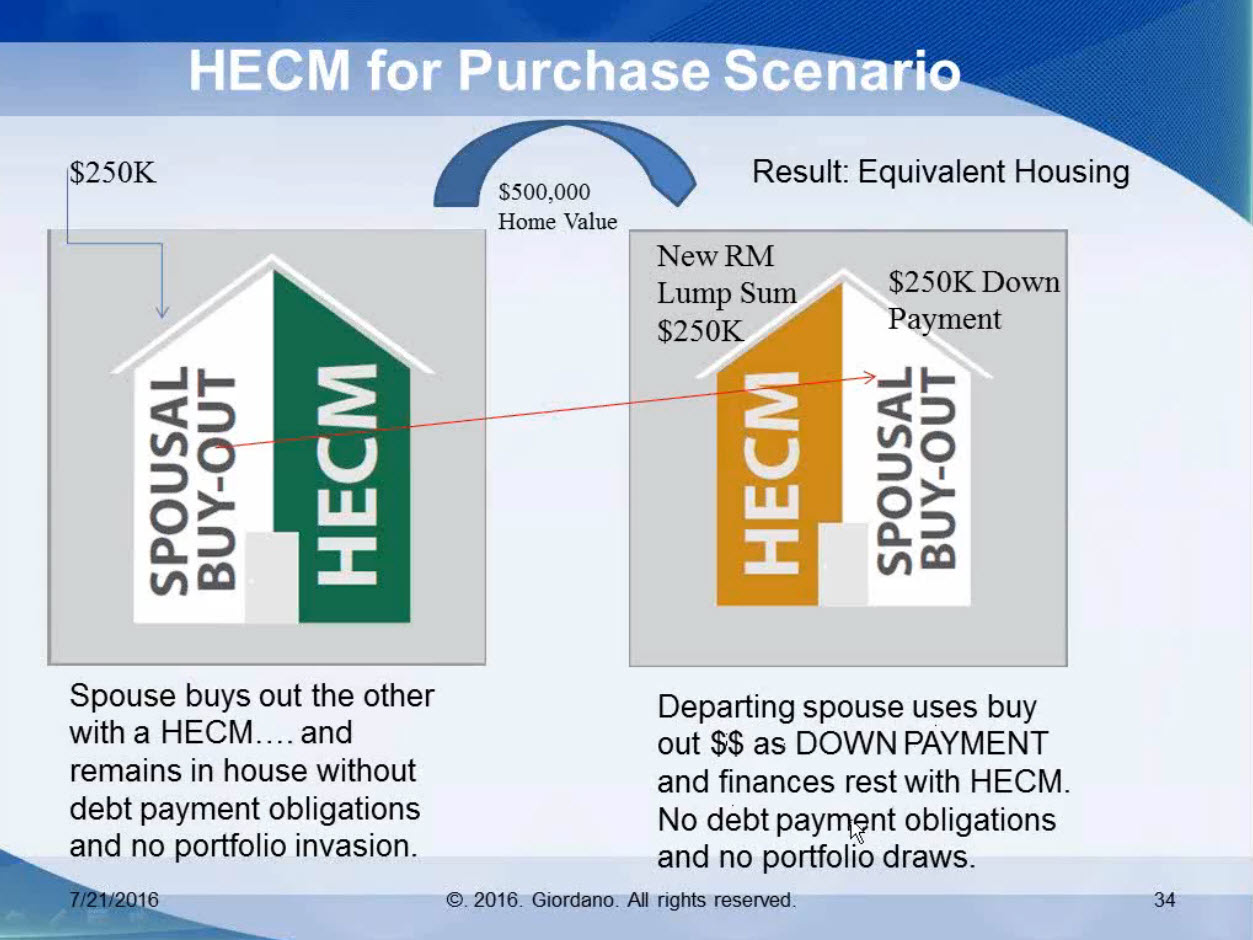

Silver divorces are a growing part of retirement for baby boomers. Financing retirement is challenging enough before splitting resources between two households. Many couples’ home is their largest financial asset, increasing the difficulty of an equitable division of assets, much less establishing a sound financial footing for their separate lives. Two ways of using a HECM reverse mortgage to help with these challenges are shown in the graphics:

Jamie Hopkins in his Forbes article ‘Silver’ Divorce Puts Strain on Retirement Income reports that “According to Barry H. Sacks, Ph.D., J.D., a member of The American College’s Longevity Funding Taskforce, an often overlooked and underutilized tool for dividing assets in silver divorces is the reverse mortgage. A reverse mortgage can be used to provide the liquidity needed to help divide the value of the home, paying out the spouse who wants the money while allowing the other spouse to remain in the home without making any mortgage payments. Monthly mortgage payments could be a huge strain on his or her retirement income each month.”

A new paper “Using Housing Wealth to Facilitate Asset Division in “Silver Divorce – Some Unconventional Uses of Reverse Mortgages” lays out a variety of ways a reverse mortgage can help a couple start their new financial lives. Barry Sacks, Mary Jo Lafaye, and Stephen Sacks, the authors, offer examples and include ways of improving post-divorce cashflow by coordinating cash from a reverse mortgage with withdrawals from an IRA or 401(k). Their paper is available here: silver-divorce-paper.

Using the older spouse’s age to the couple’s advantage:

As reported in Reverse Mortgage Daily, Dan Hultquist pointed out a strategy using what the HECM program calls non-borrowing spouses. “Since older borrowers generally can tap into a higher percentage of home equity, an older former spouse may very well wait until the younger partner leaves the home before taking out a reverse mortgage; once the younger person leaves, his or her age is no longer a part of the HECM calculus, thus netting the remaining partner more money.”

“There may be a time when it makes sense to go ahead and separate now, because they’re going to qualify for more with one borrower,” Hultquist said.

Categories: HECM, HECM Line of Credit, Retirement Spending, Reverse Mortgage

Recent Comments