How much cash would be available if a client got a reverse mortgage line of credit? There’s a straightforward process to anticipate the size of HECM reverse mortgage lines of credit. Credit lines have variable rates; fixed rate loans are also available but work a bit differently and are not covered here. HECM refers to Home Equity Conversion Mortgage, a reverse mortgage following rules set by the US Department of Housing and Urban Development (HUD) and administered by the Federal Housing Administration (FHA), bringing with it important government oversight and mortgage insurance.

Reverse mortgage calculators are available to give you a quick idea about a loan. They usually use one of several possible scenarios – such as just one lender’s margin. Calculators are available at The Mortgage Professor, reverse mortgage software companies and lender websites. This post provides insight on the variables affecting the process and how to do it yourself. Discussing a particular situation with a lender will help qualifying the client and choosing among alternatives.

The amount of cash available from a reverse mortgage depends on four things:

- The 10-year LIBOR swap rate: a long-term interest rate which serves as an estimate of compounded monthly rates expected over the next 10 years

- Lender’s margin – typically 2.25% to 3.5%

- Appraised home value

- Age of younger spouse (One spouse must be at least 62)

- “Expected Rate” is the sum of the 10-year LIBOR swap rate and lender’s margin.

- The 10-year LIBOR swap rate is available from the Federal Reserve. Look in the Interest Rate Swaps section for the 10-year number.

- The lender’s margin is often 2.25, 2.5, 2.75 or 3.0%. Lower, higher, and intermediate values may also be available. The homeowner chooses one of the offered margins.

- Once a loan is in place a short-term interest rate applies instead of the 10-year rate. The current 1-month LIBOR is added to the lender’s margin and a Mortgage Insurance Premium (MIP) of 1.25% to form the loan’s monthly compounding rate. The lender’s margin and mortgage insurance are locked in at the time of loan application, making 1-month LIBOR the only variable. The compounding rate grows the loan principal, loan balance and current line of credit. The loan grows monthly by 1/12th of the compounding rate times the loan balance. 1-month LIBOR values are available on the Wall Street Journal website.

- The home’s value won’t be officially known until an approved appraiser does an appraisal, so you may want to use a conservative value, especially if in an area where there have not been many recent sales comparable to the client’s home.

- The younger spouse’s age (18 or older) is used as they are likely to be in the home the longest. The next birth date is used if the closing date is within 6 months of the youngest spouse’s birth date, making more funds available.

Principal Limit Factor: PLF

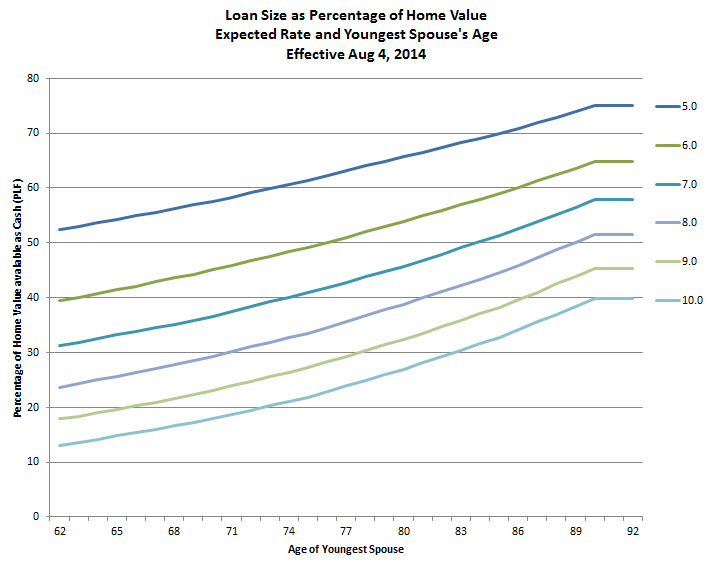

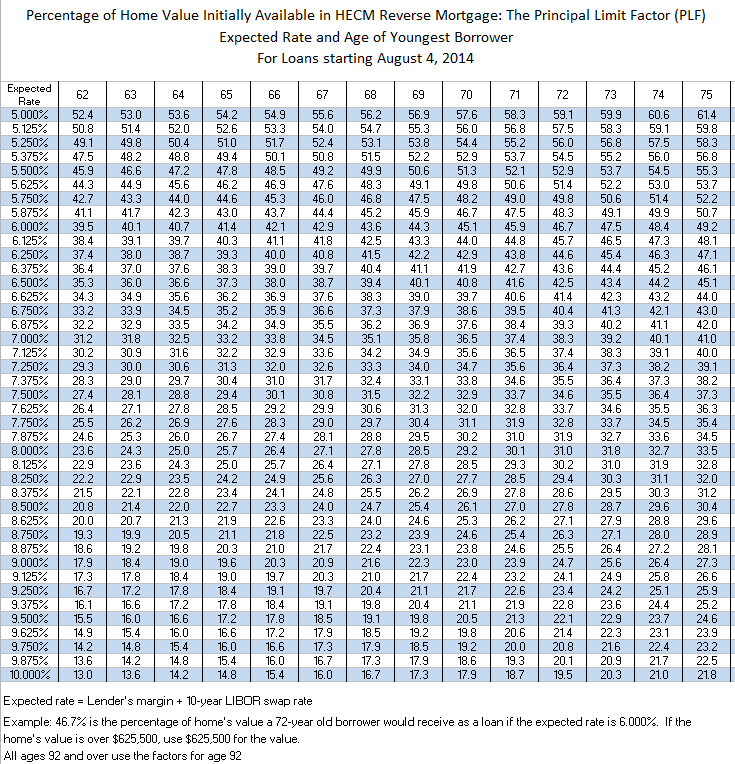

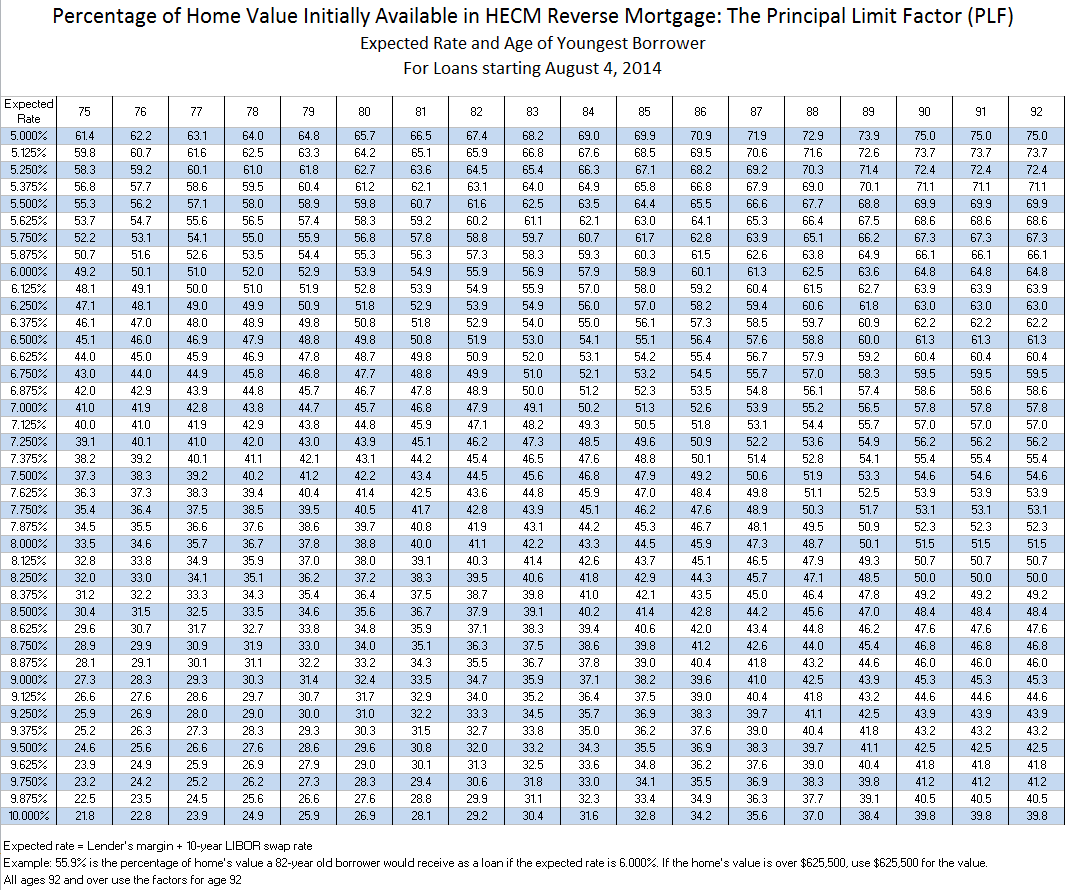

A traditional “forward” mortgage uses the concept of a loan to value ratio (LTV). In reverse mortgages this concept is called the loan’s principal limit factor (PLF). Principal Limit Factor is aptly named as it limits the loan’s initial principal. The Expected Rate and the age of the youngest spouse are all you need to look up the principal limit factor in a table. The size of the loan is simply the home’s value multiplied by the principal limit factor.

Example: Your client is 72 years old and has a $300,000 house. The 10-year interest rate (10-year LIBOR swap) is currently 3%, and assume the lender’s margin is 3%. Their loan’s “effective rate” will be 6% (3% + 3%). The lookup table with age 72 and effective rate 6% gives a principal limit factor of 46.7%. Their loan will be $140,100: 46.7% times $300,000.

An 80-year old borrower in the same $300,000 house would get a larger loan: 53.9% of their home’s value, or $161,700.

The graph shows the lookup table’s PLFs for expected rates from 5% to 10%, with lines showing different expected rates. The full table is more refined with 1/8% expected rate increments, so it has entries for 5.000%, 5.125%, 5.250% and so on. If the expected rate is under 5%, 5% is used. The current tables don’t allow for loans with expected rates over 10%.

Interest rate increases quickly reduce the size of a HECM loan. That’s seen by the spread between the lines in graph below and is more fully appreciated by looking at the graphs in another post on this blog.

The home value considered for the loan is limited to $625,500. If the home is worth $1,000,000 only $625,500 is available for loan collateral. You may see the term Maximum Claim Amount (MCA) for a loan: that’s the smaller of the home value or $625,500.

The home value considered for the loan is limited to $625,500. If the home is worth $1,000,000 only $625,500 is available for loan collateral. You may see the term Maximum Claim Amount (MCA) for a loan: that’s the smaller of the home value or $625,500.

Older borrowers get access to a larger percentage of their home’s value, as you see looking across the graph. Borrowers over 90 use the age 90 PLF. Looking down the graph you see that higher interest rates cut the percentage of the home’s available value. Both of these tradeoffs come from one underlying goal: at the end of the loan’s term the loan balance should be smaller than the house value a great majority of loans. Sufficient house value provides one way for the loan to be paid off. As these are non-recourse loans to the homeowner, when the loan balance is larger than the house’s value the lender will receive a funds from the mortgage insurance fund to close the gap. The HECM program design is intended to keep a solvent insurance fund on an actuarial basis. Balancing the needs of homeowners, lenders and the mortgage insurance pool leads to:

- The older the borrower, the more money is available. On average they won’t be in the home as long as younger borrowers.

- If interest rates are high during the term of the loan, the loan balance will compound faster and increase the chances the loan will exceed the value of the home. So high expected interest rates lead to lower initial loan amounts.

HECM Reverse Mortgage Upfront Costs

To start the process there is a required counseling session with a $125 fee and a $300 appraisal deposit. Both costs may vary. Some counseling agencies will bill the counseling fee to the closing, and may waive it based on homeowner’s income.

1) Upfront mortgage insurance premium: 0.5% or 2.5%. This guarantees that you will receive expected loan advances. The higher 2.5% is used when first year withdrawals exceed 60% of the loan, as described below.

2) Closing costs from third parties can include an appraisal, title search and insurance, surveys, inspections, recording fees, mortgage taxes, credit checks and other fees. These costs are typical of any FHA loan.

3) Origination fee. This fee pays the lender for processing your loan. HUD places caps on origination fees: up to $2,500 if your home value is less than $125,000. If your home value is more than $125,000 lenders can charge 2% of the first $200,000 of home value plus 1% of the amount over $200,000. $6,000 is the maximum HECM origination fee.

The lender can charge less, so it may be negotiable. Another way the lender gets paid is though the lender’s margin in the compounding rate applied to the loan balance: smaller margin goes with larger origination fees and vice versa. Recall that lender’s margin is part of the Expected Rate described above, and higher expected rates result in lower loan amounts. The result is you can trade off upfront and ongoing costs: upfront costs influence the amount of initial funds available and ongoing costs affect the future loan balance through the monthly compounding rate.

4) Servicing fee. Servicing is provided throughout the life of the HECM reverse mortgage. Lenders can charge a monthly service fee of no more than $35 if the interest rate adjusts monthly. In today’s market, many lenders choose to include the servicing fee in the lender’s margin part of the compounding rate so there is no servicing fee.

The loan costs may be financed by the reverse mortgage or paid out of pocket.

Limited First Year Withdrawals

There is a limit on funds that can be withdrawn in the first 12 months. The amount a borrower can take in the first year is 60% unless there are mandatory obligations that exceed that. Mandatory obligations are payments that must be made to get clear title to put the reverse mortgage in place (e.g., existing mortgages, HELOCs, liens or judgments). If mandatory obligations are more than 60% of the loan the borrower may take the total of the obligations plus 10%.

There is an additional upfront mortgage insurance cost when the first year withdrawal exceeds 60%. Mortgage insurance is 0.5% if 60% or less is withdrawn in the first 12 months and 2.5% if over 60% is withdrawn.

Examples:

- Homeowner with no mortgage can take 60% in first year; pay 0.5% MIP.

- Homeowner with $300,000 house and $250,000 prior mortgage can use 100% of the reverse mortgage right away. They pay 2.5% MIP. (They will also need to bring cash to closing).

- Homeowner with a prior mortgage at 61% of reverse mortgage can use 61% to pay off a mortgage, and draw an additional 10%. They pay 2.5% MIP.

Spouse’s Ages

The HECM program covers borrowers from age 62 and older. A younger spouse down to age 18(!) is covered, starting August 3, 2014. Spouses under age 62 are technically non-borrowing spouses. The younger they are the smaller the loan will be. This is a new area of regulation and will have additional procedures to follow before and after the loan is made.

Note: you may be able to click on graphs and tables to see a clearer copy.

Note: you may be able to click on graphs and tables to see a clearer copy.

The principal limits are available as a spreadsheet: PLF Tables Aug 4 2014. The HUD program website is the official source for this information and much more.

Here’s the PLF table when the youngest spouse is between ages 62 and 75: Note: you may be able to click on graphs and tables to see a clearer copy.

Note: you may be able to click on graphs and tables to see a clearer copy.

And here’s the PLF table when the youngest spouse is age 75 and older. All ages 90 and over use the same PLF value.

Note: you may be able to click on graphs and tables to see a clearer copy

Note: you may be able to click on graphs and tables to see a clearer copy

If you would like to print a copy of the PLF table to keep with you, download one for ages 62 and up by clicking here: Loan Size Age 62+ Starting Aug 4 2014.

The entire table from 18-year-old to 99-year-old homeowners is in the PLF Tables Aug 4 2014 spreadsheet.

Categories: HECM Line of Credit, Reverse Mortgage, Reverse Mortgage General, Uncategorized

Great overview of reverse mortgages. This post was referred to in Wade Pfau’s The Hidden Value of a Reverse Mortgage Standby Line of Credit. I am providing CE on this topic in 2016, and will certainly direct attendees to your site.